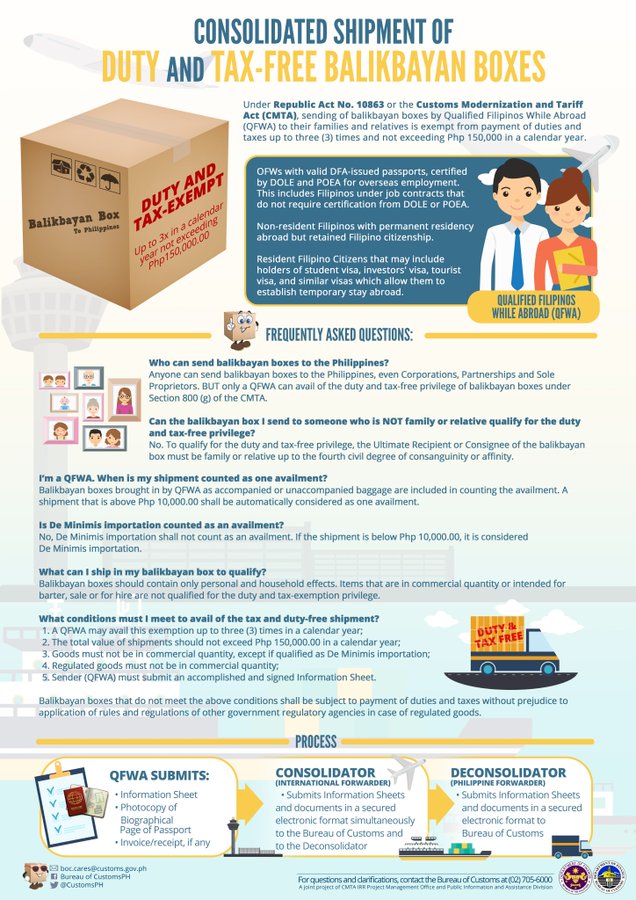

Qualified Filipinos While Abroad (QFWA) can send balikbayan boxes up to three times in a calendar year provided that the total value shall not exceed 150,000 pesos according to the Bureau of Customs.

Here is BOC’s latest press release regarding guidelines on duty and tax-free balikbayan boxes posted on May 8, 2019 on its website.

BOC reiterates guidelines on duty and tax-free balikbayan boxes

The Bureau of Customs today reiterated the guidelines in availing the duty and tax-free privilege of consolidated balikbayan boxes.

It may be recalled that BOC has issued Customs Memorandum Order (CMO) No. 18-2018 providing the guidelines on the availment of the privilege by qualified Filipinos on their consolidated shipment of balikbayan boxes.

The CMO allows that instead of the mandatory copy of Philippine passport, overseas Filipino workers (OFW) must submit other documents to show proof of Filipino citizenship such as photocopy of pertinent page of the Philippine passport with personal information, picture and signature, or in case of dual citizenship, a photocopy of foreign passport with personal information, picture and signature, and copy of proof of being a dual citizen.

Other documents such as permanent resident ID or equivalent document in other countries, overseas employment certificate/Overseas Workers Welfare Administration (OWWA) card, work permit, unified government ID issued by the Department of Labor and Employment (DOLE), and any other equivalent document in lieu of a birth certificate would also be required.

Qualified Filipinos availing of the P150,000 duty and tax-free privilege are not required to submit the commercial invoices of the goods contained in the balikbayan box. Invoices are to be submitted only if it is available.

For freight forwarders or deconsolidators, they are required to submit the information sheet in 3 legible copies, where the first copy to be kept by the sender, and the third copy to be given to the deconsolidator and has to be forwarded to the Bureau together with other documentary requirements, which will serve as the packing list of the balikbayan box.

On the other hand, under Section 423 of the Republic Act No. 10863, otherwise known as Customs Modernization and Tariff Act (CMTA) , “no duties and taxes shall be collected on goods with a value of P10,000 or below.”

Section 800 (f), meanwhile, states that returning residents or those who have stayed in a foreign country for a period of at least 6 months shall have tax and duty-free exemption on personal and household effects, provided that it shall not be in commercial quantities and it is not intended for sale or for hire.

Returning residents may also avail the privilege provided that it is limited to the FCA or FOB value of (1) P350,000 for those who have stayed in a foreign country for at least ten (10) years and have not availed of this privilege within ten (10) years prior to returning resident’s arrival; (2) P250,000 for those who have stayed in a foreign country for a period of at least five (5) but not more than ten (10) years and have not availed of this privilege within five (5) years prior to returning resident’s arrival; or (3) P150,000 for those who have stayed in a foreign country for a period of less than five (5) years and have not availed of this privilege within six (6) months prior to returning resident’s arrival.

Any amount in excess of the above-stated threshold shall be subjected to the corresponding duties and taxes under the CMTA.

Section 800 (g) of the CMTA stipulates that residents of the Philippines, OFWs or other Filipinos while residing abroad or upon their return to the Philippines shall be allowed to bring in or send to their families or relatives in the Philippines balikbayan boxes which shall be exempt from applicable duties and taxes provided that balikbayan boxes should only contain personal and household effects.

Balikbayan boxes may be sent up to 3 times in a calendar year provided that the total value shall not exceed P150,000.

Any amount in excess of the allowable non-dutiable value shall be subject to the applicable duties and taxes.